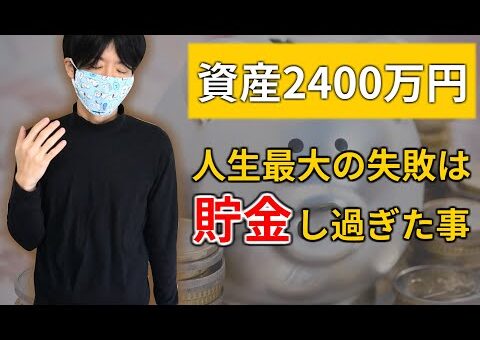

節約が最強の副業なワケ #shorts #節約 #貯金 #副業

節約が最強の副業なワケ #shorts #節約 #貯金 #副業  ムームードメインで安心!身に覚えのない請求への明確な対応策

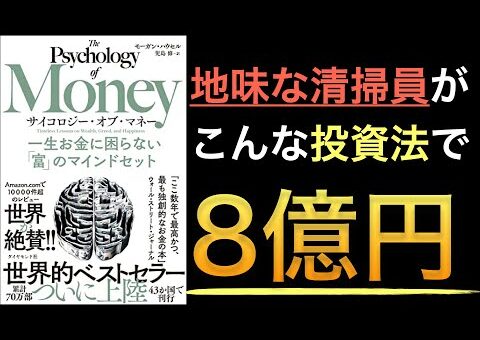

ムームードメインで安心!身に覚えのない請求への明確な対応策  【最高の基礎教材】本気でお金持ちになりたいなら簿記とFPを学ぶべき5つの理由【お金の勉強 初級編】(アニメ動画):第5回

【最高の基礎教材】本気でお金持ちになりたいなら簿記とFPを学ぶべき5つの理由【お金の勉強 初級編】(アニメ動画):第5回  第250回 【不安解消!】今の日本で子育てするための「基本戦略」と「ファイナンス法8選」【お金の勉強 初級編】

第250回 【不安解消!】今の日本で子育てするための「基本戦略」と「ファイナンス法8選」【お金の勉強 初級編】  【不動産投資】副業禁止の会社で始める方法3選

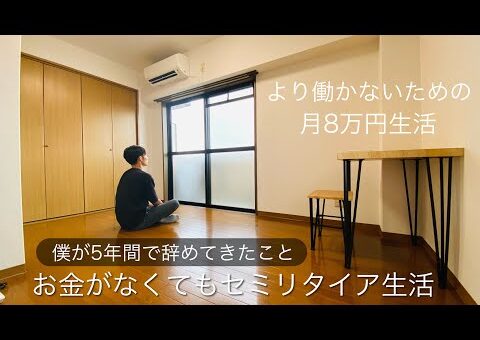

【不動産投資】副業禁止の会社で始める方法3選

ムームードメイン更新料:賢い管理でオンラインアイデンティティを守る

ムームードメイン ムームー...

ムームードメイン ムームー...

https://www.youtube....

ムームードメイン ムームー...

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

ムームードメイン ムームー...

ムームードメイン ムームー...

ムームードメイン ムームー...

https://www.youtube....

https://www.youtube....

ムームードメイン ムームー...

ムームードメイン ムームードメインでの銀...

ムームードメイン ムームー...

https://www.youtube....

https://www.youtube....

ムームードメイン ムームー...

最新の動向:水原一平容疑者の法的対応と謝...

https://www.youtube....

ムームードメイン ムームードメインとさく...

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

ムームードメイン ムームー...

https://www.youtube....

ムームードメイン ムームー...

https://www.youtube....

ムームードメイン ムームードメインへのド...

ムームードメイン ムームー...

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

競馬予想なら!【競馬最強の...

どこよりもWiFi 【どこ...

https://www.youtube....

https://www.youtube....

賭博疑惑が浮上 大リーグで活躍する大谷翔...

発売日2024-05-03 10:00:...

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

キャピキシル配合のスカルプエッセンス フ...

https://www.youtube....

https://www.youtube....

https://www.youtube....

ムームードメイン ムームー...

https://www.youtube....

発売日2024-05-08 10:00:...

https://www.youtube....

https://www.youtube....

ムームードメイン ムームー...

ムームードメイン ムームー...

ホームページ作成サービスで夢を現実に ホ...

https://www.youtube....

https://www.youtube....

ムームードメイン ムームー...

チャットレディ:自宅で叶え...

最短翌日着 便利な冷凍弁当...

ムームードメイン ムームー...

ヒックス ミノキシジル &...

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

ムームードメイン ムームー...

https://www.youtube....

https://www.youtube....

ムームードメイン ムームー...

https://www.youtube....

ムームードメイン ムームー...

ムームードメイン ムームー...

花粉症対策:快適な春を取り...

フルボ酸・リデンシル配合!【リジュン】 ...

https://www.youtube....

https://www.youtube....

ムームードメイン ムームー...

ムームードメイン ムームー...

薬用 発毛促進剤【モウダス】 モウダス ...

最新情報は公式サイトから⇒<薬用育毛剤ア...

https://www.youtube....

ムームードメイン ムームー...

https://www.youtube....

ムームードメイン ムームー...

https://www.youtube....

https://www.youtube....

山本陽子のおススメ理由はズバリ! 清楚で...

https://www.youtube....

ムームードメイン ムームー...

https://www.youtube....

ムームードメイン ムームー...

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

ムームードメイン 身に覚えのないクレジッ...

ムームードメイン ムームー...

https://www.youtube....

https://www.youtube....

ポケモンアプリの魅力を全て紹介! 「ポケ...

京都旅行:古都の魅力を全身で感じる旅 京...

日常の疑問: 知的好奇心を刺激する学びの...

ワンピースキャラクターのおススメ理由はズ...

今日は何の日:毎日がもたらす驚きと発見 ...

楽天くじ:毎日がもっとワクワクする 楽天...

ドラクエ10の魅力を全て紹介!あなたも冒...

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

山本リンダとは 山本リンダは日本の歌手で...

https://www.youtube....

https://www.youtube....

ムームードメイン &nbs...

https://www.youtube....

https://www.youtube....

https://www.youtube....

ムームードメイン クーポンのご利用方法に...

https://www.youtube....

ヒロセ通商【LION FX...

マトリックストレーダー マ...

ムームードメイン ムームードメイン キャ...

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

https://www.youtube....

ムームードメイン ムームー...

ムームードメイン ムームー...

https://www.youtube....

ムームードメイン ムームー...

ムームードメイン ムームー...

https://www.youtube....

ムームードメイン ムームー...

ムームードメイン キャンペーン概要 ムー...